Republished by Blog Post Promoter

The sinking of the titanic (owned by J.P. Morgan) was ‘the tip of the iceberg’. The titanic sinking pulled off 4 of the greatest criminal plots in history — all at the same time!

The sinking of the titanic (owned by J.P. Morgan) was ‘the tip of the iceberg’. The titanic sinking pulled off 4 of the greatest criminal plots in history — all at the same time!

1) with the sinking of the ship, JP Morgan murdered all of his business competition at once — 3 of the 4 wealthiest men in the world — all of whom opposed the Federal Reserve Act that would give Morgan control of the entire money supply of the United States.

2) squashed the invention of “free energy” by Nikola Tesla ensuring private control of energy revenue forever, i.e. oil, coal, gas, electricity, etc..

3) guaranteed the passage of the “Federal Reserve Act” to establish his private bank and control all of the gold, money supply and property of the united states.

4) saved his ‘White Star’ ship line from bankruptcy by collecting a fraudulent insurance payment on the titanic.

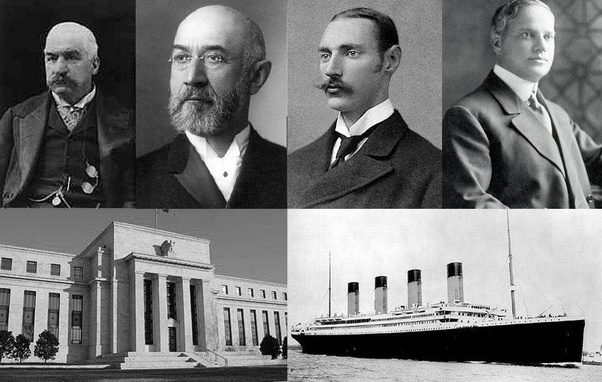

PHOTO — (1st Row: JP Morgan, Joseph Bruce Ismay, John Jac ob Astor and Benjamin Guggenheim. 2nd Row: The Federal Reserve and the Titanic)

ob Astor and Benjamin Guggenheim. 2nd Row: The Federal Reserve and the Titanic)

As youngsters, we’re all told the infamous story of the Titanic, the supposedly indestructible ship that sunk on its maiden voyage. We’re all familiar with the story: the ship left Southampton, England, headed for New York City on April 10, 1912.

Four days into the voyage, at 11:40pm on April 14, 1912, the Titanic struck an iceberg and sank at 2:20am, “resulting in the deaths of 1,517 people in one of the deadliest peacetime maritime disasters in history [12].”

Bad luck, we’re all led to believe. No one saw the iceberg and so the infallible ship sank. Bummer…

But few of us ever think that through. Forget, for a moment, the story we’re all fed. Does it make sense? My point is that just because we’re told a story when we’re young, doesn’t mean we should simply accept it as absolute truth.

Let’s take a look at some of the facts surrounding the sinking of the Titanic:

As youngsters, we’re all told the infamous story of the Titanic, the supposedly indestructible ship that sunk on its maiden voyage. We’re all familiar with the story: the ship left Southampton, England, headed for New York City on April 10, 1912. Four days into the voyage, at 11:40pm on April 14, 1912, the Titanic struck an iceberg and sank at 2:20am, “resulting in the deaths of 1,517 people in one of the deadliest peacetime maritime disasters in history [12].”

Bad luck, we’re all led to believe. No one saw the iceberg and so the infallible ship sank. Bummer…

But few of us ever think that through. Forget, for a moment, the story we’re all fed. Does it make sense? My point is that just because we’re told a story when we’re young, doesn’t mean we should simply accept it as absolute truth.

Let’s take a look at some of the facts surrounding the sinking of the Titanic:

1. The unsinkable Titanic sunk…on its maiden voyage. How could this unsinkable ship sink? On its first trip, no less! That alone is quite remarkable/intriguing.

2. “Captain E.J. Smith ignored multiple iceberg warnings from his crew and other ships.” Getting from England to New York as fast as possible was goal number one, at the behest of his boss, Joseph Bruce Ismay, Managing Director of the White Star Line. Ismay had pressure from his boss, J.P. Morgan, owner of White Star Line [3]. By the way, Ismay survived the catastrophe.

3. Speaking of J.P. Morgan, he had his very own private suite and promenade deck on the Titanic. He was supposed to be on that fateful maiden voyage but canceled passage [8]. Coincidence or part of Morgan’s plan?

4. Once the Titanic struck the iceberg, the captain and his crew used white flares to signal distress. Unfortunately,white flares are not the color used to signal distress; red flares are always used to show distress. So the closest ship, the Californian, ignored the flares, assuming it was a celebratory signal, rather than an emergency [7]. Oops…

5. “All ships must carry sufficient lifeboats for the number of passengers on board. The Titanic did not [7].”

6. “About three million rivets were used to hold the sections of the Titanic together. Some rivets have been recovered from the wreck and analysed. The findings show that they were made of sub-standard iron. When the ship hit the iceberg, the force of the impact caused the heads of the rivets to break and the sections of the Titanic to come apart. If quality iron rivets had been used, the ship may not have sunk [7].”

7. “The belief that the ship was unsinkable was, in part, due to the fact that the Titanic had sixteen watertight compartments. However, the compartments did not reach as high as they should have. White Star Line did not want them to go all the way up because this would have reduced living space in first class [7].”

8. Killed on the sinking ship — along with 1,514 other people — were Benjamin Guggenheim, Isa Strauss and John Jacob Astor. Astor was, at the time, believed to be the wealthiest man on the planet. Guggenheim and Strauss weren’t far behind Astor. And these three powerful men opposed the Federal Reserve.

(PHOTO LEFT) An angry JP Morgan yelling at photographers. He hated having his picture taken.As an aside to the above facts, let’s take a look at an additional dimension to the dynamic between J.P. Morgan and John Jacob Astor. Both Morgan and Astor invested large sums of money in the brilliance of Nikola Tesla, a genius inventor who gained notoriety during the late 19th/early 20th century. Morgan’s primary concern with Tesla was making money. Astor and Tesla, however, were good friends [9].

(PHOTO LEFT) An angry JP Morgan yelling at photographers. He hated having his picture taken.As an aside to the above facts, let’s take a look at an additional dimension to the dynamic between J.P. Morgan and John Jacob Astor. Both Morgan and Astor invested large sums of money in the brilliance of Nikola Tesla, a genius inventor who gained notoriety during the late 19th/early 20th century. Morgan’s primary concern with Tesla was making money. Astor and Tesla, however, were good friends [9].

“Col. John Jacob Astor, owner of the Waldorf-Astoria, held his famous dining-room guest [Tesla] in the highest esteem as a personal friend, and kept in close touch with the progress of his investigations. When he heard that his researches were being halted through lack of funds, he made available to Tesla the $30,000 he needed in order to take advantage of Curtis’ offer and build a temporary plant at Colorado Springs[11].”

So what was the big deal about Tesla? Well, “Tesla had claimed to be able to send electrical energy without wires before the turn of the century, and he envisioned people all around the globe sticking rods into the earth to extract that energy — free …. After Tesla admitted to financier J.P. Morgan that an experimental tower on Long Island was meant to send power as well as message, his public career ended …. Corporate moguls who were interested in creating monopolies and metering electrical power blackballed him [10].”

Now let’s take a look at a few of the above facts that, when taken together, may paint quite a different picture of the tragedy of the Titanic:

1. J.P. Morgan owned White Star Line ships. J.P. Morgan was also the main conspirator behind the creation of the Federal reserve banking system. He was supposed to be on the ship but canceled at the last moment.

2. John Jacob Astor, along with Benjamin Guggenheim and Isa Strauss, were three very wealthy and powerful men, all of whom were vehemently against the creation of the Federal Reserve, and were quite outspoken on the matter. Morgan viewed Astor and Co. as a huge obstacle. These three men died when the Titanic — a ship built by J.P. Morgan’s White Star Line — hit that infamous iceberg and sank.

3. J.P. Morgan and John Jacob Astor both funded Nikola Tesla, who created a way to generate an infinite amount of electrical energy. Tesla planned to allow people to access that energy for free, but Morgan squashed Tesla because he wanted to profit from energy, not give it away. Astor, Tesla’s good friend, seemed to have deep pockets for Tesla. Not good for Morgan.

4. Once Astor, Guggenheim and Strauss were dead, there was no more public outcry against the Federal Reserve. It passed congress and was signed into law the following year on December 23, 1913. In addition, now Tesla’s funding was wiped away, his friend in Astor gone.

You must admit, all of this is extremely interesting. Could Morgan have created this plot to kill off his biggest opponents? Did Morgan “whack” Astor because he was getting in his way on too many wealth and power-generating projects?

Admittedly, there are some holes in this interesting theory. For example:

1. Why wouldn’t Morgan have simply had Astor, Guggenheim and Strauss shot? That certainly would have been easier than sinking an entire ship. Then again, then there would have been intense investigations into their murders. When multi-billionaires turn up dead, no stone is left unturned.

2. How could Morgan guarantee Astor, Guggenheim and Strauss would be on the ship? Maybe there were behind-the-scenes events, put in place by Morgan, to ensure those men would be on the ship. We’ll never know.

3. Moreover, how could Morgan be sure Astor, Guggenheim and Strauss would go down with the ship and not get off onto lifeboats? Maybe Morgan knew well of the truly high character of Astor: “Colonel Astor was another of the heroes of the awful night. Effort was made to persuade him to take a place in one of the life-boats, but he emphatically refused to do so until every woman and child on board had been provided for, not excepting the women members of the ship’s company [4].” Apparently, Guggenheim and Strauss did the same.

4. Why would J.P. Morgan have believed that unless Astor, Guggenheim and Strauss were killed, his coveted Federal Reserve Act wouldn’t have passed? It seems strange that these three men would have had the combined political power to diffuse Morgan & Co.’s clandestine plans.

However, even with the doubt these questions raise in this theory, one cannot help but look upon the story of the Titanic with suspicion.

Is it just a coincidence that J.P. Morgan owned White Star Line, the company that produced the supposedly unsinkable Titanic, and that it went down with his enemy, John Jacob Astor, as well as Federal Reserve opposers Guggenheim and Strauss?

And is it merely coincidence that Morgan and Astor both funded Nikola Tesla, whose innovations could have been either the greatest gifts to mankind or the greatest wealth generators for the few, depending upon who controlled them?

Could the Titanic have been the most ingenious assassination in history?

THE TITANIC INSURANCE SCAM

by John Hamer

In 1908, financier J.P. Morgan planned a brand new class of luxury liners that would enable the wealthy to cross the Atlantic in previously undreamed-of opulence. The construction of the giant vessels, the ‘Olympic’, the ‘Titanic’ and the ‘Britannic,’ began in 1909 at the Harland and Wolff shipyard in Belfast, Ireland.

In 1908, financier J.P. Morgan planned a brand new class of luxury liners that would enable the wealthy to cross the Atlantic in previously undreamed-of opulence. The construction of the giant vessels, the ‘Olympic’, the ‘Titanic’ and the ‘Britannic,’ began in 1909 at the Harland and Wolff shipyard in Belfast, Ireland.

Unfortunately for Morgan and his personal bank balance, this money-making venture went a little awry. The Olympic, the first one of the three sister-ships to be completed was involved in a serious collision with the British Royal Navy cruiser, HMS Hawke in September 1911 in Southampton a few weeks after its maiden voyage and had to be ‘patched-up’ before returning to Belfast to undergo proper repair work.

In hindsight, it does seem strange that although the Olympic, the first of the ‘sisters’ to enter service, was never given the publicity her younger sister, the Titanic, enjoyed the following year Why would that be?

In the meantime a Royal Navy inquiry into the accident found the Olympic at fault for the collision and this meant that the owner, White Star Line’s insurance was null and void. The White Star Line was out of pocket to the tune of at least £800,000 (around $90m today) for repairs and lost revenues.

However, for Morgan and the White Star Line, there was even worse news.

It is believed that the keel of the ship was actually twisted and therefore damaged beyond economic repair, which would have effectively meant the scrapyard. The White Star Line would have been bankrupted, given its precarious financial situation..

According to Robin Gardner’s book, ‘Titanic, the Ship that Never Sank?‘

the seeds were sown for an audacious insurance scam – the surreptitious switching of the identities of the two ships, Olympic and Titanic.

In his well-documented work, Gardner presents a long series of credible testimonies, indisputable facts and evidence, both written and photographic, that suggest that the two ships were indeed switched with a view to staging an iceberg collision or other unknown fatal event.

According to Gardner, “Almost two months after the Hawke/Olympic collision, the reconverted Titanic, now superficially identical to her sister except for the C deck portholes, quietly left Belfast for Southampton to begin a very successful 25-year career as the Olympic. Back in the builders’ yard, work progressed steadily on transforming the battered hulk of the Olympic into the Titanic. The decision to dispose of the damaged vessel would already have been taken. … Instead of replacing the damaged section of keel, longitudinal bulkheads were installed to brace it”.

How significant then in the light of this statement, that when the wreck of the Titanic was first investigated by Robert Ballard and his crew after its discovery in 1987, the first explorations of the wreckage reportedly showed (completely undocumented in the ships original blueprints) iron support structures in place which appeared to be supporting and bracing the keel.

This was never satisfactorily explained either at the time or subsequently but would certainly be significant if correct and there is absolutely no reason to believe that it is not correct, as it was reported by the puzzled Ballard himself who of course at that time knew nothing (and probably still does not even now) about the alleged switching of the two ships’ identities.

————————————————————————————————–

References:

1. http://www.world-mysteries.com/doug_titanic1.htm

2. http://www.titanic-whitestarships.com/Owners2.htm

3. http://www.rense.com/general70/goodc.htm

4. http://www.logoi.com/notes/titanic/women_children_first.html

5. http://www.pacinst.com/terrorists/chapter5/titanic.html

6. http://www.museumstuff.com/learn/topics/Jesuit_conspiracy_theories::sub::The_Sinking_Of_The_Titanic

7. http://www.historyonthenet.com/Titanic/blame.htm

8. http://hubpages.com/hub/The_Titanic_Historical_Society

9. http://www.reformation.org/nikola-tesla.html

10. Begich & Manning, “Angels Don’t Play This HAARP” p. 12-13

11. O’Neil, “Prodigal Genius” p. 175

12. http://en.wikipedia.org/wiki/RMS_Titanic